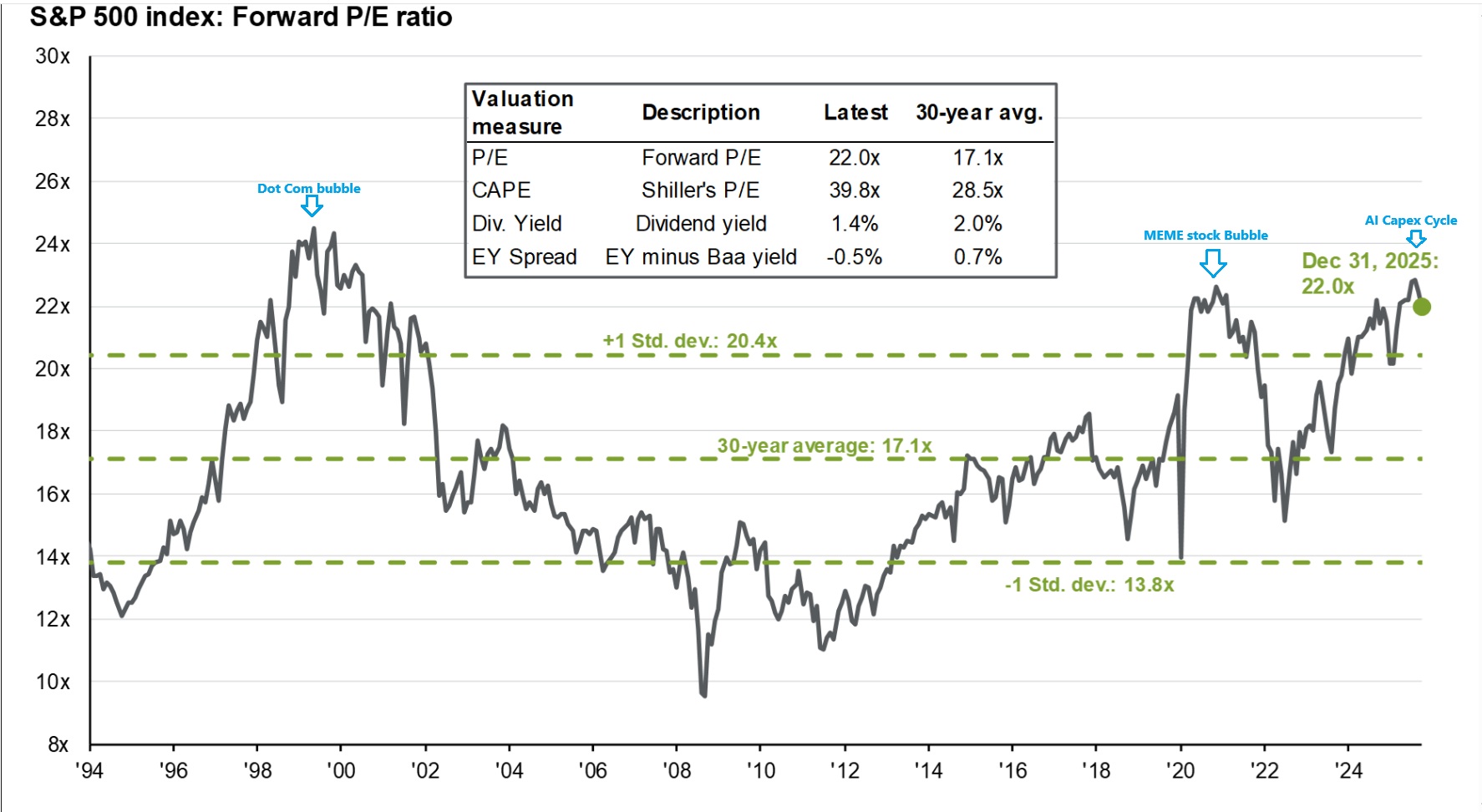

Model 01

Equity Risk Premium

Daily Calculated Spread — Earnings Yield minus Risk-Free Rate

Loading…

Expensive (−2%)

Fair (3%)

Cheap (8%)

Historical Average: 3.2%

S&P 500 Earnings Yield

--%

10-Year Treasury Yield

--%

Commentary last updated · January 12, 2026

Why is this important?

The Equity Risk Premium represents the excess return that investing in the stock market provides over the risk-free rate (10-Year Treasury). It is a fundamental metric for valuation at the index level — the higher the spread, the more investors are compensated for taking on equity risk.

What is occurring?

The spread has turned negative, denoting very expensive valuations. Note that this model relies on trailing earnings without dividends, making it a backward-looking diagnostic. While useful for historical baselines, see Model 02 below for a comprehensive, dividend-adjusted view.

Critical Watch Level

10Y Yield > 4.5%