Executive Summary

- Revolving credit (credit card balances) seldom falls during economic growth cycles — making the current decline a notable signal.

- We saw a 2.05% quarterly decline — the sharpest quarterly drop in consumer credit card balances since the pandemic shock, and approaching the −2.75% drop at the peak of the 2009 financial crisis.

- While top-line consumer credit growth appears to have stabilized, the current range-bound trajectory suggests a pivot toward precautionary deleveraging — indicating the American consumer is prioritizing balance sheet repair in response to perceived employment fragility.

This data series is valuable for informing one's understanding of aggregated spending trends and consumer sentiment. The major caveat: one does not look in the rear-view mirror while driving. The series tells us where we've been, not where we're headed.

Consumer Uncertainty Builds and Sustains

Below is a composite of consumer sentiment survey data plotted alongside revolving credit balances. Survey data provides a better forward-looking read versus aggregate spending data. December's sentiment reading bounced off multi-decade lows, but remains sub-60 — a threshold that marked the lows during both the GFC and the 2011 technical near-recession.

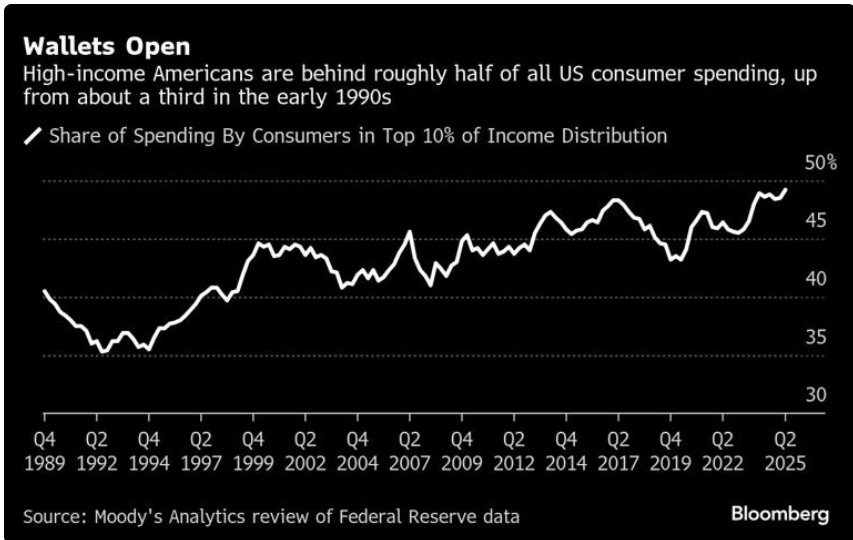

Similar to the weakness seen in 2011 — where a technical recession was never formally declared — we are seeing the same consumer pessimism, but this time it is translating into actual changes in spending habits. The "K"-shaped economy is predicated on further equity market gains, as consumption is now driven in large part by the highest income cohorts. The dichotomy in the economy is plain to see.

Chaos Theory Outlook

Current market sentiment suggests that a combination of Federal Reserve rate cuts and substantial tax refunds will bolster consumer spending through Q1 2026 — a narrative already reflected in asset prices. While history shows tax relief can stimulate spending or cushion a downturn, it rarely prevents a recession entirely; the 2001 Economic Growth and Tax Relief Reconciliation Act serves as a prime example. In my view, the real driver remains the AI capex cycle. The resulting wealth effect from equity performance will likely sustain our "K-shaped" economy until this investment cycle reaches its peak.